Written by: Sr. KC Law, Principal & Valuer at Action Real Estate & Valuers

Here is a short story about John (fictional character) and his house buying journey to help us in explaining 26 must know real estate terms.

All the terms are defined in the real estate glossary at the end. The terms are hyperlinked to one another, so you can click back and forth!

John plans to get married next year and is on a house buying journey…

There are several options he can consider but because he wants a ready property so he decided to buy from the (1)sub-sale market. After calling up a few real estate agents and going for several viewings, he finally selected a (2) leasehold condo unit with a purchase price of RM500K. As this was his first time buying a property, he told the real estate agent that he would need some time to consider the purchase. He wanted to know if the price quoted by the real estate agent is truly what the property is worth.

John then calls up his ex-schoolmate who works with a (3) valuation company to verify the offer. He provides to his friend details such as, the property name, exact address, (4) built-up area, some information about the specifications of the property and even some pictures he took during the viewing to his friend to verify the property’s current value.

After some calculations and comparisons with other recent transacted property prices around the same street, his friend’s feedback is that the (5) market value of the property is RM550K. So this means the purchase price of RM500K is in fact 10% below market value. Feeling assured, John went ahead and pays an (6)earnest deposit of 3% to the registered real estate agency and signed a (7)“Letter of Intent to Purchase” or booking form. With the booking form issued by the real estate agency in hand, he then goes to several banks recommended by his real estate agent to source for a bank loan to finance this property.

On assessing his loan request, the banks would consider his monthly income and capacity to make the monthly repayments before granting the loan approval. Since this is John’s first property purchase, he is eligible for 90% (8) margin of financing and there were 2 banks which were willing to offer him RM450K loan. After comparing the banks’ offer, he chooses the loan that offered a lower (9) interest rate and better terms and conditions. After finalizing the bank offer for his loan, he then needs to appoint a bank panel lawyer to prepare the (10) loan agreement. Legal fee here is borne by John.

Next, he is also advised to appoint a (11) conveyancing lawyer to prepare the (12) Sales and Purchase agreement (SPA). To execute the Sale and Purchase agreement, John is required to pay the seller another 7% to make up the 10% down payment and the balance, i.e. the 90% will be paid through bank financing.

Since the property is a relatively new condo with a (13) master title, the sale will be by way of (14) deed of assignment. If the unit has an individual (15) strata title then it will be by way of memorandum of transfer (Form14A). The seller is paid the balance 90% within 90 days from date of signing of SPA or (16) consent from developer and/or (17) relevant authorities (whichever is later) with an extension of 30 days carrying an interest rate of 8%.

John was informed that the Ministry of Finance’s Valuation and Property Services Department, also known in Bahasa Malaysia as (18) Jabatan Penilaian dan Perkhidmatan Harta (JPPH) will assess the property value independently for calculation of (19) stamp duty to be charged. This is done by the SPA lawyer by the process of (20) adjudication. Since John is a first time home buyer, there is great news for him; he gets to enjoy stamp duty exemption! See glossary below to find out how to calculate stamp duty and also how much John would have to pay after his exemption.

In the event the market value assessed by the Collector of Stamp Duties is higher than the SPA price (i.e. purchasing price, in this case RM 500k), the stamp duty chargeable will be based on the market value instead of the SPA price. It is important to ensure the SPA document is stamped, as a document which is not stamped or insufficiently stamped is void or (21) unenforceable for that reason alone.

The bank that offers the loan for the property will also usually appoint a panel valuation company to confirm the property’s current market value before the release of loan. In this case, if the bank values the subject property as RM500K or more, then the bank will finance RM450K or 90% of the SPA price. However, if the bank values the property less than RM 500K, what would then happen? Answer: He will not be able to get RM 450K financing!

If John had not done his due diligence/ homework of checking out the current market value of the condo before putting his foot down to purchase, John would have to fork out a lot more money. For example, if the bank valuation of the condo is RM450K, then the bank will only finance 90% of RM450K which is only RM405K. John will have to top-up the shortfall of RM45K in cash! The valuation fee for the valuation report on the condo is borne by John.

If the (22) vendor (the right term to refer the seller as) has not paid up his bank loan in full, John’s SPA lawyer will need to get the (23) redemption sum that states the outstanding amount owing to the vendor’s bank. After paying the redemption sum and other (24) encumbrances on the property the remaining sum will be paid to the vendor to (25)discharge the property. Upon full payment of RM500K John will claim (26) vacant possession of the condo he has purchased. Finally, just before the big move, John will need to apply for new electricity account and water supply account by paying the deposits for these utilities. After which he is all ready to move in and occupy the premise.

Real Estate Terms/Glossary:

1. Sub-Sale

Existing properties that are available and are usually occupied by owners or renters, or vacant.

2. Leasehold

An owner of a leasehold property is not the owner of the land upon which the building is erected, but is a lessee of the land for a period varying from three years to 99 years (the maximum period of lease permitted by the National Land Code 1965). Opposite to leasehold (sort of), is what is known as freehold, it basically means permanent and absolute tenure of land or property with freedom to dispose of it at will. (added in for completion)

3. Valuation

Valuation establishes an opinion of value utilizing an objective approach based on facts related to the property, such as age, square footage, location, cost to replace, etc.

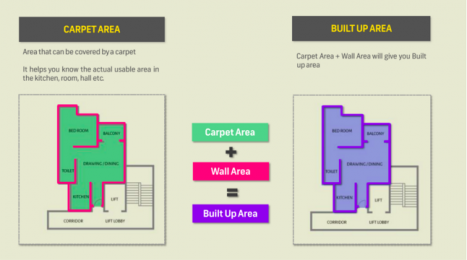

4. Built-up area

Built up area is the carpet area plus the thickness of outer walls and the balcony. Check out the diagram below from housing.com, which shows what the built up area constitutes.

Diagram was taken from housing.com

5. Market value

Market Value is the estimated amount for which a property should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion. In simpler terms, it means the price an asset is able to fetch in the marketplace.

6. Earnest deposit

Earnest deposit is something like a “booking fee”, given by the purchaser to the seller when he/she makes an offer to purchase the property. This is a payment to show that you are serious about buying the property. It is counted towards the down payment, and refundable if the offer is not accepted. The earnest deposit payment should be made payable to the real estate agency. Once the SPA is signed, this earnest deposit will be the real estate agent’s commission from the seller.

7. Letter of Intent to Purchase

A Letter of Intent to Purchase, also known as a booking form is a document outlining an agreement between two or more parties before the Sale and Purchase agreement is finalized. The letter provides an outline of the proposed terms of the transaction so the parties can negotiate before committing to a contract. It is needed to minimize misunderstanding and document progress towards a sale. Since this intent letter is not a binding contract, which means the property owner can still sell the property to someone else. It’s also a great way for a buyer to help secure financing.

8. Margin of Financing

The margin of financing depends on a few things, the value of the property, your income and your repayment capability. The amount of financing provided by a financial institution depends on the market value (for completed properties only) or purchase price of the house, whichever is lower. For example, if a property is priced at RM500,000 and the Margin of Financing is 90%, the amount of own money is RM50,000. Want to know more about how to get a housing loan? Read “Getting A Housing Loan”

9. Interest rate

The fee charged by a lender to a borrower for the use of borrowed money, usually expressed as an annual percentage of the principal; the rate is dependent upon the time value of money, the credit risk of the borrower, and the inflation rate.

10. Loan agreement

Also known as a loan or credit facility agreement or facility letter. An agreement or letter in which a lender (usually a bank or other financial institution) sets out the terms and conditions (including the conditions precedent) on which it is prepared to make a loan facility available to a borrower.

11. Conveyancing

The process of transferring property between a buyer and a seller. In real estate, conveyancing involves drawing up and carrying out a written contract that sets out the agreed purchase price and the date of transfer, as well as the obligations and responsibilities of both parties.

12. Sales and Purchase Agreement (SPA)

SPA is actually a written contract representing the seller and buyer in a real estate transaction. It lists down all the terms and conditions of the purchase as well as the role of both parties. In the event there is a default from any one party, the termination and indemnity clause in the agreement will provide protection.

13. Master title

A title, or title deed, indicates the owner of a property. In most cases, every property during the stages of development and construction will be under a single Master Title.

14. Deed of Assignment (DOA). (if title is not issued)

DOA is a legal document that transfers the interest of the owner of that interest to the person to whom it is assigned, the assignee. When ownership is transferred, the deed of assignment shows the new legal owner of the property. Sign DOA, When land still under master title.

15. Strata Title

Strata Title is the separate property deed for each unit in a sub-divided property (multi-storied building or a number of buildings on a piece of land that have common facilities administered by a management committee). These can include: apartments, condominiums, townhouses,etc.

16. Consent from developer

Get the consent of the developer to the sale of the property to the new buyer and to undertake

the registration of the property in the name of the new buyer.

17. Relevant authorities

The SPA of such schemes may have restriction on the buyer selling the property. i.e. it could not be sold within a stipulated period or without the consent of the government. The title to the property may have restrictions. (the restrictions could be read from the title or search of the title) e.g. property cannot be transferred or charged without State consent.

18. Jabatan Penilaian dan Perkhidmatan Harta (JPPH)

Valuation and Property Services Department of Ministry of Finance, JPPH advises the Federal Government, State Government, Statutory Body and Local Authority in Malaysia on matters pertaining to the valuation of real estate and property services. Besides this, JPPH also provides information on sale or transfer of real estate to valuers, appraisers or estate agents who are registered with the Board of Valuers, Appraisers and Estate Agents Malaysia

19. Stamp duty

For the transfer/assignment (if no individual title is issued), based on the adjudicated value by

the Stamp Office:

For 2017

First RM 100,000 – 1%

RM 100,001- RM 500,000 – 2%

RM 500,001 and above – 3 %

For 2018

First RM 100,000 – 1%

RM 100,001- RM 500,000 – 2%

RM 500,001 – RM 1,000,000 – 3%

RM 1,000,000 and above – 4%

For first time home buyers, the government has come out with an initiative to provide stamp duty exemption to reduce the cost of home ownership.

Up to RM 300, 000 – 100% exempted

>RM 300,000 – as per rates set out above.

Let’s try to calculate how much John would have to pay..

Price of property RM 500,000

First RM 100,000 -(1%) RM 1,000

RM 100,001 – RM 500,000 – (2%) RM 8,000

Total (without exemption)= RM 9,000

Exemption= RM 1,000 + RM 4,000 = RM 5,000

Means that he still needs to pay a balance of RM 4,000.

20. Adjudication

The purpose of adjudication is to ensure that the instrument is duly stamped to protect the parties to the contract in respect of the admissibility of the instrument as evidence in court during a civil proceeding. An instrument which is not duly stamped is not admissible in court as evidence.

21. Void or Unenforceable

A void contract is a formal agreement that is illegitimate and unenforceable from the moment it is created. There is some overlap in the causes that can make a contract void and the causes that can make it void and unenforceable contract is a valid contract that cannot be fully enforced due to some technical defect.

22. Vendor

The seller of a property.

23. Redemption sum

The outstanding amount owing to the Vendor’s bank (“Redemption Sum”). Where the Redemption Sum exceeds the Purchase Price or the Balance Sum, additional provisions are required to be made for payment of the amount in excess by the Vendor.

24. Encumbrance

A claim against a property by a party who is not the owner. Mortgages, easements and liens are examples of some encumbrances that can apply to real estate assets.

25. Discharge

Removing a debt by making full payment. A mortgage discharge is a document formally specifying that a mortgage debt have been paid.

26. Vacant possession

It is usual for the contract for the sale of a property to contain a provision confirming the property is to be sold with vacant possession. Vacant possession is an obligation on the Seller to make the property available on completion in a state in which the Buyer can physically and legally occupy it.

There you have it, 26 real estate terms you would encounter during a property transaction! Share it with others and subscribe to our blog for more articles like this!

Action Real Estate copyrights reserved. Do not reproduce or copy the content of this post without first obtaining our consent.

About the Author

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyor Malaysia and Member of Malaysia Institute of Estate Agents.