Written by: Sr. KC Law, Principal & Valuer at Action Real Estate & Valuers

We have been frequently asked this question about the Malaysia property market – New development, Auction or Sub sale, which market is for me? In this week’s blog entry, we will summarize the pros and cons of each property market and briefly outline the typical profile of buyers in each market.

There are typically two main reasons for purchasing real estate, i.e. for investment or for own stay. The consideration factors for both are completely different and should not overlap.

If you intend to purchase for your own stay, your emotional feelings come into play when making a decision.

For example, do you like the neighborhood, are you happy with the renovation work of the house, do you like the front porch, do you like the fittings in the house etc.

On the other hand, when buying a property for investment, one should never let emotions come into play, only good numbers!

These numbers we are referring to are the property price, rental yield and its potential for capital appreciation.

Before hunting for a property, it is important to be clear of your purpose first!

To reiterate, 3 of Malaysia’s property markets are:-

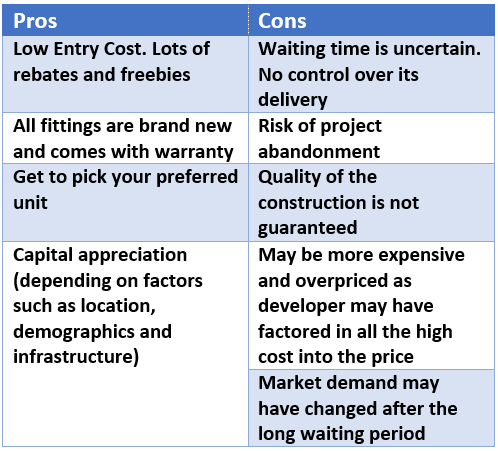

Property market #1: New Development

New development, also known as the primary market is usually the choice of new/young buyers because of the low entry cost of new development projects.

The entry cost is typically between RM5k to RM10k, with most of the other cost such as legal fees, sales and purchase agreement covered by the developer.

To stay competitive, many developers also offer rebates and freebies to their purchasers.

Therefore, for new buyers that have limited savings to qualify for a sub sale purchase, this is the likeliest entry into the market.

From a buy-to-stay perspective, buying from the primary market gives you the privilege of choosing your preferred unit, it also ensures that everything within the property is brand new and the buyer can be assured that everything is in its best condition.

On completion of the project, the property is in move in condition and any defects are covered by warranty from the developer.

From an investor’s perspective, buying from the primary market may be beneficial in terms of higher potential for capital appreciation after the entire project reaches completion.

Since we can expect construction cost and property prices to rise at least in proportion with inflation, buying it in its early phase may give you an advantage.

However, this is highly dependent on many other factors such as the location, demographics, infrastructure and other developments around the area, it pays to do your due diligence of the area and surroundings before buying into any new development projects as they are not without its disadvantages as well.

For one, it is the more risky option because the project completion can be delayed since today’s cost of materials, labor, land and statutory compliance is very much higher.

So if you are buying into a new project, there is risk of the project having a construction period of more than 3 years, sometimes some projects even get abandoned mid way.

All this waiting period is risk with interest, and as buyers you will have no control over its delivery.

Also, due to the rising costs, these costs are factored into the price of the property, often times making them more expensive than its actual value, therefore causing less appreciation than expected.

The finish product’s quality is not guaranteed and may differ from that of the sample house, what you see in the show room may not always be what you will get.

Other than that, after delivery of keys, there is also the possibility that the market demand of the area may have dropped or changed after the waiting period of 3 years or more.

For instance, soon after the completion of your condo, several other high rise might have followed, causing an over supply. Some investors will be stuck with not being able to sell/rent out their unit.

Property market #2: Auction

Next, let’s discuss what the auction market entails, also known as the tertiary market.

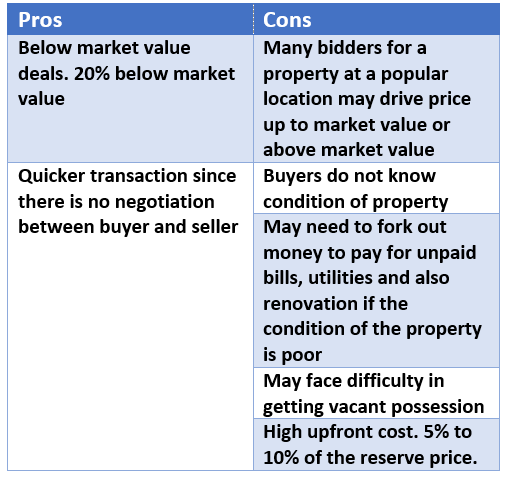

Auction properties are usually priced at 20% below market value.

An investor or a person buying to stay may be able to get a below market value deal at the auction market and transactions are typically faster since there is no need for negotiation between buyer and seller.

However, auction properties are very well publicized in the market these days not only by auctioneers but also by property agents, it is no longer easy to get a good property at bargain price.

Auction properties at prime location will also attract many bidders. This will eventually drive up the price to market value and sometimes even above market value.

The entry cost is high, as bidders need to prepare a deposit of 5-10 percent of the reserve price and be ready to top up the difference in deposit after a successful bid.

Even if a buyer manages to purchase it at below market value, the condition of auctioned properties are usually in very bad state.

The money saved from purchasing a cheap property may have to be used for major renovation works, and also pay for unpaid taxes, bills, utilities and assessments.

Interested bidders are also unable to view the property before making a decision.

Moreover, the buyer may face difficulty in obtaining vacant possession of the auctioned property and may even need to go through lengthy procedures to obtain a court order to vacate the occupant of the property.

With all that has been said, it may still be a good option to consider for properties in unpopular areas that have untapped potential or non general purpose properties that attract fewer buyers from the market.

As you can already tell, purchasing an auction property has many uncertainties, hence making it risky.

Property market #3: Sub Sale

Lastly, lets discuss about the sub sale market, also known as the secondary market.

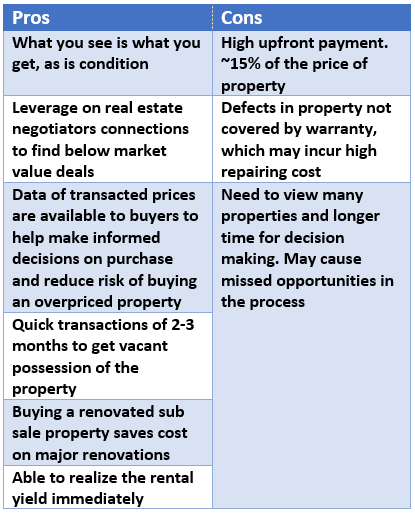

When buying a property from the developer, you can only picture what it will be like when the project completes.

For a completed property, you can have a real look and feel of the property, what you see is what you get. You can see everything about the unit, from the view, the renovation works done to the property, the surrounding area, demographics of the area and etc.

On top of that, data of transacted prices will already be available to you either through your trusted real estate negotiator or through your research on various property portals. With so much of information available, a buyer is able to make informed decisions on their purchase and reduce the risk of purchasing an overpriced property.

It pays to be good friends with real estate negotiators as they may even help you secure below market value deals in the sub sale market, why not leverage on their network and connections? You do not even need to pay the negotiator, since the seller/vendor pays the commission (for most parts of Malaysia).

The lower the property price is, the higher the rental yield and return on investment will be. Besides, compared to new developments, the transaction is way quicker as it usually takes only about 2-3 months to get all the paperwork done and get vacant possession of the property.

From a buy-to-stay perspective, many home buyers nowadays look for renovated sub sale property as it can save them money on renovation as cost of building materials have also gone up over the years.

As for property investors, purchasing property from the sub sale market allows you to realize the rental yield immediately as you will be able to start letting out your property once you have vacant possession of the property.

For all the reasons stated above, the sub sale market is many seasoned investor’s favorite property market.

However, the same cannot hold true for new/young home buyers as it requires a high upfront payment, namely 10% down payment, legal fees, stamp duty, valuation fees, just to name a few (approximately 15% of the property price).

Other than that, buyers of sub sale properties need to spend a lot of time viewing different properties before making a decision on a purchase.

Sometimes the time taken for decision making may cause a genuinely interested buyer to miss out on the sale due to other buyers who have made a decision quicker. Also, with sub sale properties, there is no warranty on defects of the property, you buy a property as is.

Many times older sub sale properties may come with defects which may not be immediately apparent such as a piping defect, electrical defect or termite infestation. This may require extensive repairing work which may be costly.

Fortunately, there is good news! End of year 2016 and year 2017 is an interesting time for buyers (investors/people buying to stay) as there are many “new” sub sale properties in the market.

These may be properties that are just being handover to the owners. Many of these properties were purchase before 2014 under the developer interest bearing scheme (DIBS). So it is not uncommon to see many brand new properties for sale at competitive prices in the market now.

In conclusion, buying a property depends on the purpose of your purchase (investment/buy to stay), financial readiness and risk appetite.

According to Warren Buffet, “Risk comes from not knowing what you are doing”. Therefore, it pays the best dividend to equip yourself with the skills and knowledge necessary to manage and minimize the risk of buying property.

Finally, always engage a qualified real estate agent/negotiator for all your property transactions! (Find out “Are you dealing with a certified Real Estate Negotiator?“)

New Development, Auction or Sub Sale, which is your preferred property market?

Action Real Estate copyrights reserved. Do not reproduce or copy the content of this post without first obtaining our consent.

About the Author

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyor Malaysia and Member of Malaysia Institute of Estate Agents.