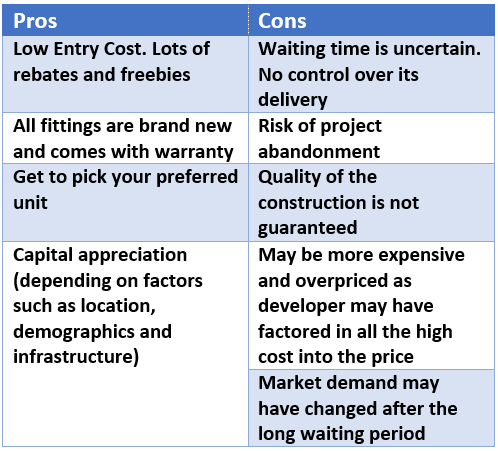

In recent years due to the economic slowdown, we see a significant increase in the number of properties entering into the auction property market. Many homeowners lose their holding power and start defaulting on their home loans. Many of these units are brand new, never-lived-in units purchased during the era of Developer Interest Bearing Scheme (DIBS). At that time, it was so easy to make an entry into the property market. Buyers only need to fork out as low as RM 3000 to start owning a property. Under this scheme, buyers are not required to pay the mortgage until the property is completed. Many of these buyers probably purchased it thinking that they could flip it later for a profit. Unfortunately, due to the soft property market, they are unable to find a buyer. Also, some buyers during the point of purchasing the property may not have adequately assessed their ability to repay the loan. Once they receive their keys 3 years later, they are suddenly faced with huge loan repayments that they are unable to afford. Finally, these properties end up being auctioned.

According to an auction specialist, Leslie Low, in 2017, about 2500 properties are auctioned off every month. This is about 50% increase since 2013; during that time, there were only about 1000-1500 auctioned properties every month.

What does this mean for you? If you are looking for a property for investment or for your own stay, whether you are an experienced buyer or a first-time buyer, there are thousands of properties below market value up for grabs! If you’re looking for a great value deal, read on!

What are auction properties?

Auction properties are residential or commercial properties that go up for sale through a competitive bidding process. The buyer who makes the highest bid during the auction will get to buy the property. Once the hammer falls, a legal binding contract will be set between the seller and the purchaser.

Where do auction properties come from?

When property owners start defaulting their bank loans, the bank will send reminders to borrowers and introduce penalty by increasing the interest rate and charging overdue penalty cost. If borrowers are unable to service the interest or repay the principal over a period of more than 3 to 6 months, the borrower’s loan will be classified as a Non-Performing Loan (NPL). These properties will be moved to foreclosure or the auction department of the bank. These properties will then be sold to the open market via public auction for the bank to recover the loan given out to the defaulted borrowers.

What are the benefits of bidding for (and buying) auction properties?

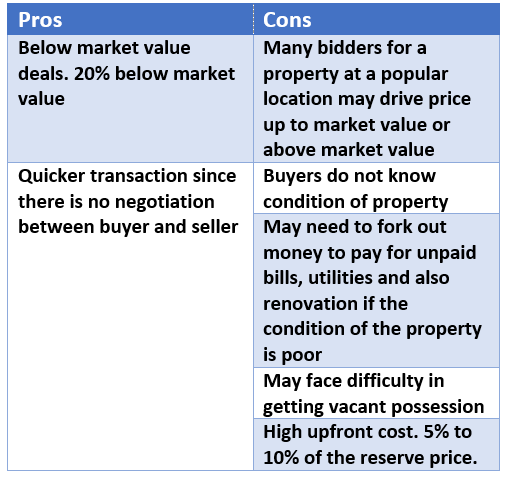

Auction properties are priced at Forced Sale Value, which is usually at 20% below market value. That means buyers stand to enjoy a 20% discount off a particular property!! Should there be no bidder for the auction property, the reserve price (the lowest price at which the property can be sold) will be lowered by another 10% in the next auction date. Sometimes, you might even be able to get an auction property at 50% below market value. Besides this, you can own a property very quickly by buying from the auction market because there is no negotiation process between the buyer and the seller.

Documents required for bidding

For individuals:

- A photocopy of your IC

- A bank draft or cashier’s order equivalent to 10% of the reserve price

- Additional funds to pay for the shortfall in the deposit of the successful bid vs the reserve price.

- Authorization letter (if you are bidding on behalf of someone)

For companies:

- A photocopy of director’s IC

- A bank draft or cashier’s order equivalent to 10% of the reserve price

- Additional funds to pay for the shortfall in the deposit of the successful bid vs the reserve price.

- Board of Director’s resolution

- Form 24 and 49

- A certified true copy of the company’s Memorandum and Articles of Association (M&A)

- Authorization letter (with company letterhead and company stamp, signed by at least 1 director)

- IC and photocopy IC of the person authorized to bid

What is the process of buying an auction property?

- You must be at least 18 years of age to be an eligible bidder.

- Select your desired auction property based on the auction list or recommendations provided by your auction agent.

- Conduct an official title search with the relevant Land Office and make general enquiries with the developer and management office. You may engage your agent to do this for you by paying a small fee.

- Go to the location and conduct an external inspection of the property to ascertain the current condition of the property. Do not rely only on the description of the property. You may engage your agent to do this for you.

- Conduct due diligence checks on the property depending on what type of property you are bidding for – LACA/non-LACA. You may engage your agent to do this for you.

For property on master title or Loan Agreement Cum Assignment (LACA), these properties are usually auctioned by banks through a private auction house eg. Public Auction House Sdn Bhd, Ng Chan Mau & Co. Sdn Bhd, Ehsan Auctioneers Sdn Bhd, etc

Due diligence checks required are:

- Outgoings consisting of quit rent, assessment, maintenance charges, sinking fund, TNB, SYABAS, Indah water and developer.

For Property with individual title/strata title (non-LACA), properties will be auctioned by High Court or Land Administrator.

Due diligence checks required are:

- Title search to ensure no caveat (it is a formal legal notice to the world that you have an interest in a particular property or land)

- Outgoings consisting of quit rent, assessment, maintenance charges, sinking fund, TNB, SYABAS and Indah water.

- Once you have decided to bid for the property, get a copy of the Proclamation of Sale (POS) and Condition of Sale (COS). Your agent will download a copy and explain the important clauses in the POS and COS to you.

- Register yourself as a bidder with the bank via the auction agent servicing you.

- Pre-qualify and pre-arrange financing for the selected property with your bank.

- Take note of the auction’s date, time and venue.

- Prepare a bank draft, 10% of the reserve price, as stated in the POS and COS.

- List down other costs not covered by the bank. These are usually stated in the POS and COS.

- Ensure you reach the auction venue at least 30 minutes earlier and register at the auctioneer registration counter. You will be given a bidders card with a number during the bidding. Your agent should attend the bidding with you, or if you are unable to bid on your own, you may also authorize your agent to bid on behalf of you. (You will need to provide an original authorization letter, a photocopy of your IC and bank draft to your agent)

- Before the bidding process, the auctioneer will read out some important clauses in the POS and COS and some information about the property. He will then announce the commencement of the auction.

- During the bidding, you or your agent bidding on behalf of you will raise the bidding card to indicate the bidding price. The bidding will stop when the highest price is called out 3 times by the auctioneer and no higher bids are made. At the fall of the hammer, the property is sold.

- (Recommended) Ensure you prepare additional cash or bank draft to top up the difference in deposit sum between successful bidding price and reserve price. This must be paid after the auction should you be the successful bidder.

- If you are the successful bidder, you will then have to sign the Contract of Sale. The balance of purchase price must be paid within 90 (for LACA) or 120 days (non-LACA) as per the POS and COS.

- Contact the bank you have selected and pre-arranged to finance the balance 90% of your purchase price.

- Should the current occupant refuse to vacate the property, apply for a distress order and get a court order through a lawyer to demand vacant possession.

- For unsuccessful bidders, your deposit will be refunded immediately after the auction.

- Do take note that if you are the successful bidder and later change your mind on the purchase, your deposit will be forfeited.

In the coming years, we may also have some added convenience and transparency to this process as bidders will soon be able to bid online with e-Lelong! Read more here & here.

What are the risks of buying auction properties and how we can minimize it?

As with any type of transaction, buying from the auction has its own risks. Know the risks involved and take a calculated risk before going to an auction.

-

You do not get to view the property’s internal condition, and if the property is in bad shape, you may have to fork out extra money for repair and renovation works

If the property is tenanted, you may try to ask the tenant if they allow you to take a quick look at the property. If the property is owner-occupied, you may also ask the permission of the owner to take a quick view of the property, and at the same time, you might also wish to check if they are already prepared to vacate the property. Do expect some hostile treatment. You may also wish to consider speaking to the neighbours, they may be able to give you some valuable information.

-

The property may have many outstanding utility bills left unpaid and you may have to quantify it

Before the auction date, do ensure you or your agent goes to the relevant utility offices, such as Tenaga Nasional Berhad, SYABAS, management office, with a copy of the POS to check on the outstanding bills.

-

You may have trouble evicting previous occupants

Once you are the official owner of the property, you can then engage a lawyer to distress the occupant and then apply for a court order. Always check if the property is occupied before the auction.

-

The property may have a caveat

Ensure you or your auction agent do a title search for properties with title.

Whether you’re a property investor or a first time home buyer, the auction property market has something for everyone. Familiarize yourself with the process, ensure you do a thorough investigation of the property to get a better picture of the costs involved to ensure you get a great deal!

Keen to explore the opportunities in the auction property market?

Contact us at 03-7785 1888. Let us know what you’re looking for and our agents will contact you with a list of auction properties based on your specifications.

Like our Facebook page for more content like this ->https://www.facebook.com/actionrealestate.my/

Action Real Estate copyrights reserved. Do not reproduce or copy the content of this post without first obtaining our consent.

About the Author

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyors Malaysia, Member of Malaysia Institute of Estate Agents and Member of Business Valuers Association of Malaysia.