Written by: Sr. KC Law

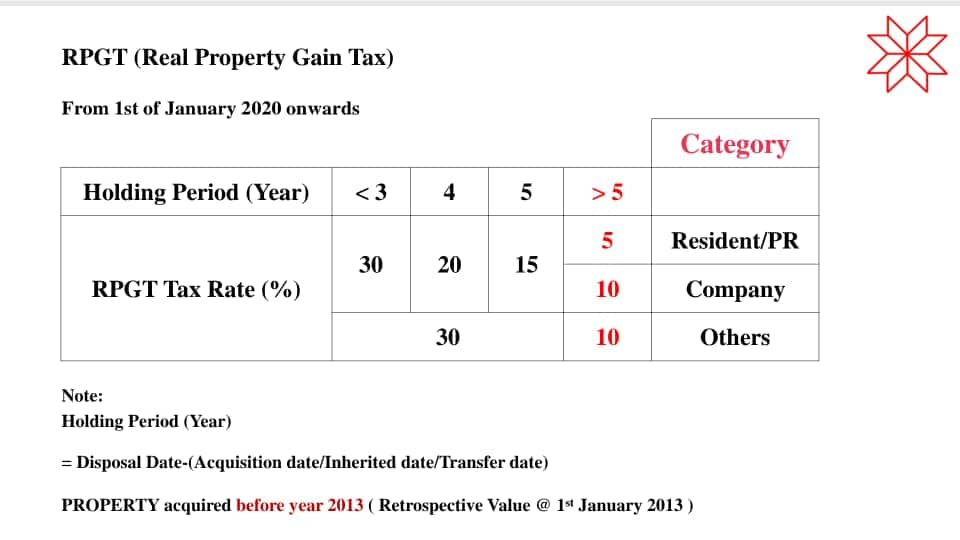

When we sell any of our property from the year 2019 and beyond, we will need to pay “Real Property Gain Tax (RPGT)”. When we buy property, we pay “Stamp Duty” at the market value of the property, to grasp the importance of stamp duty planning, read our article: Buying Property and Stamp Duty Planning. In this article, we highlight the prudent actions needed for effective RPGT planning.

It is crucial to know the facts and make informed decisions; being ignorant of the laws and regulations is extremely costly and time-consuming to rectify.

Example 1

Mr Lim inherited a 3-storey shophouse in Kuala Lumpur from his late father via a valid Will. (Read more: Getting a Property Valuation On Your Inheritance, When and Why?)

He may plan to sell it immediately or 5 years after getting the “Grant of Probate” from the High Court.

Basic equations:

- Acquisition Date = Date of demise

- Holding period in year(s):

Disposal Date – Acquisition Date

- Chargeable Gain:

Disposal Price – Acquisition Price – Allowable Expenses

Read more: Real Property Gains Tax (RPGT) in Malaysia

From the above, the inherited 3-storey shophouse Acquisition Price or Market Value on the date of demise is unknown since there is no property valuation done.

Mr Lim is street smart and prudent, so he plans to determine the unknown Market Value at Date of demise by himself (Do It Yourself = DIY) to save cost.

Here are probably some DIY methods he might have considered:-

Method 1. Get an indicative price for similar property 3-storey shophouses in similar location advertised in the local newspaper(s) for the property by property agents. Cut out the advertisement and use it as Acquisition Price.

Method 2. Get the advertised prices for a similar property advertised in online property advertising portals. Print it out and use it as Acquisition Price.

Method 3. Call up several active real estate agents/negotiators in the area of the inherited property. Record down their verbal average indicative prices as Acquisition Price.

The above DIY methods seem to be very simple and cost-effective to determine the Acquisition price (Market Value) at Date of demise (inherited date).

The question is – Is this Acquisition Price (Market Value) at Date of demise derived from above methods valid or can it be used as Market Value of the property for submission to Inland Revenue Board (IRB) for RPGT tax purposes when Mr Lim sells his 3-storey shophouse immediately or in the future?

The answer is, unfortunately NO.

Why can’t these pieces of evidence be adopted?

The market value from the above methods is just hearsay indicative asking prices and cannot be used for RPGT tax calculation nor submission.

It is an offence punishable by imprisonment and/or fine should anyone who is not a Registered Valuer with the Board of Valuers, Appraisals, Estate Agents and Property Managers of Malaysia were to sign a valuation report stating the market value of any property for any specific date in Malaysia.

Now, let’s look at the correct and legal ways available to property owners/beneficiaries like Mr Lim who wish to get their property market value on the inherited date or date of demise or transfer date.

Situation 1- Owners/Beneficiaries who plan to sell/dispose of the property immediately after getting the “Grant of Probate”.

- Engage a Registered Valuer to conduct a property valuation and draw up a valuation report of market value at the date of demise.

- The date of demise is taken as the date of acquisition or date of valuation.

- The Holding Period is Date of Disposal – Date of Acquisition.

Situation 2 – Owners/Beneficiaries who plan to keep the inherited property after getting the “Grant of Probate” or sell after 5 years.

- After getting Grant of Probate, transfer/ register the beneficiaries name(s) into the title by Memorandum of Transfer (MOT) or Deed of Assignment for a non-title property.

- Engage a Registered Valuer to conduct a property valuation and draw up a valuation report on the date of registration of the title or assignment date on the Deed of Assignment for a non-title property.

- The inherited property will now have a market value at acquisition date which is the date of registration on the title or date of Deed of Assignment.

In the above example, our objective is to get market value for the property/inherited property at acquisition date under 2 situations that is valid and can be used in the future for RPGT tax planning purposes.

The above RPGT planning is a prudent and recommended way for all property owners who plan to sell their property for 2019 and after.

Example 2

What happens if owners of property who sold their property but felt that the RPGT calculated by the authority does not reflect the market value?

They can make an appeal with a detailed property valuation report from a Registered Valuer on the affected property within the specified appeal date.

However, this is a reactive approach which may in some cases not work in the favour of the owners.

The understanding of the above will help property owners/beneficiaries overcome the challenges in managing RPGT proactively when selling their property.

Should you need further advice or clarification. Please contact us at 03-7785 1888 or email us at action.v1039@gmail.com

About the Author

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyors Malaysia, Member of Malaysia Institute of Estate Agents and Member of Business Valuers Association of Malaysia.

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyors Malaysia, Member of Malaysia Institute of Estate Agents and Member of Business Valuers Association of Malaysia.