Written by: Sr. KC Law

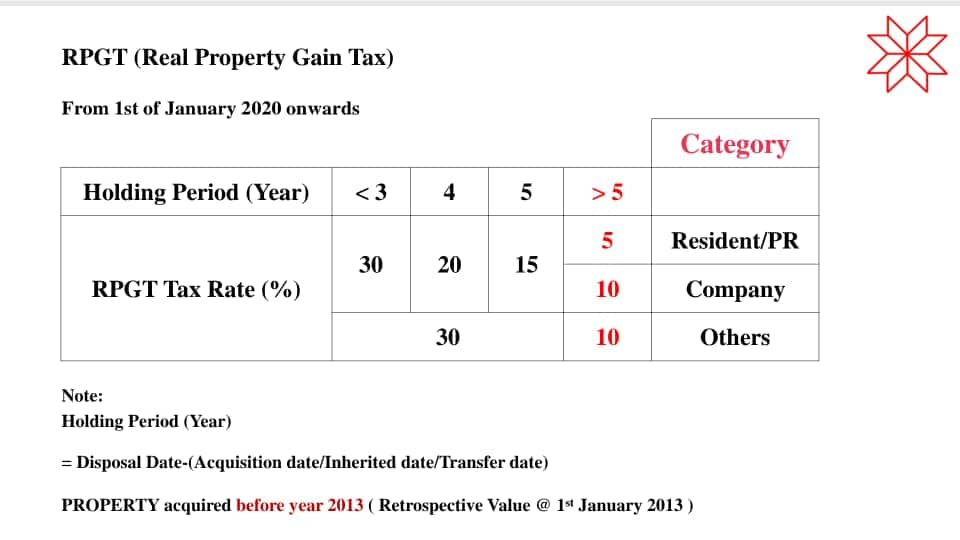

In our earlier article Selling Property and Real Property Gains Tax (RPGT) Planning, we discussed the prudent approach property owners can adopt to manage RPGT effectively when they decide to sell their property.

What consideration is there for a property buyer to take note of when buying a property?

Every purchaser has to pay Stamp Duty when buying any property, except specific property categories exempted by the government.

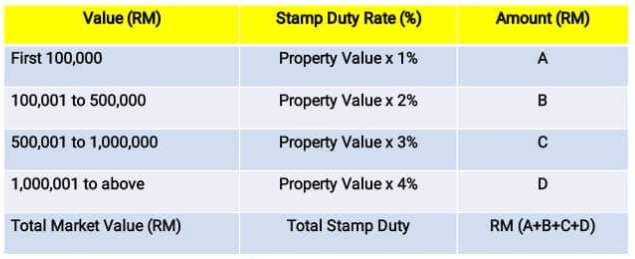

The Stamp Duty payable by purchasers depends on the property value and calculated based on the rate below:

Example

When a purchaser buys a property at RM1.5M, what is the Stamp Duty the purchaser needs to pay?

The Stamp Duty based on the above rate is:

1st RM100K @1% = RM1K

Above RM100K to RM500K @2%= RM8K

Above RM500K to RM1M@ 3%= RM15K

Above RM1M to RM1.5M @4%= RM20K

Stamp Duty payable is =RM1K+RM8K+RM15K+RM20K=RM44K.

What is the basis of the Stamp Duty calculation apart from the schedule rate?

The stamp duty payable by a purchaser of a property is based on the market value of the property at the date of transaction.

Case 1

Buyer A buys a property at market value of RM1.5M.

Jabatan Penilaian dan Perkhidmatan Harta (JPPH) authority values its market value to be RM1.5M.

Stamp duty payable is RM44K.

NO action needed because it is valued at market price.

However, what can Buyer A do if JPPH authority computes the market value of the property as RM2M when the fair market value is RM1.5M thus increasing stamp duty chargeable to RM64K, which is RM20K more?

Buyer A can make an appeal to have the property revalued by the authority, submitting with the appeal a full Property Valuation Report prepared by a private Registered Valuation company justifying with solid evidences why RM1.5M is the correct and accurate fair market value.

Case 2

Buyer B buys a property below market value at RM1M from a desperate seller.

The fair market value is RM1.5M

How much stamp duty does the purchaser have to pay?

RM24K or RM44K?

The answer is RM44K. Why RM44K?

Stamp duty chargeable/computation is based on market value.

Case 3

Buyer C buys a property above market value at RM2M from his neighbour for his son who plans to get married next year.

The fair market value is RM1.5M

How much stamp duty does Buyer C have to pay?

RM44K or RM64k?

The answer is RM64K. Why?

Stamp duty computation is based on the higher of the two that is Sales and Purchase Agreement (SPA) value.

Remember this: You pay stamp duty when you buy property at market value or SPA price.

Should you need further advice or clarification. Please contact us at 03-7785 1888 or email us at action.v1039@gmail.com

About the Author

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyors Malaysia, Member of Malaysia Institute of Estate Agents and Member of Business Valuers Association of Malaysia.

Sr. KC Law is a Registered Valuer, Estate Agent and Property Manager with The Board of Valuers, Appraisers, Estate Agents and Property Managers (BOVEAP) of Malaysia. KC Law is also an electronic engineer registered with the Board of Engineer Malaysia (BEM) and received his engineering training from Tunku Abdul Rahman College Malaysia and later at Hatfield Polytechnic United Kingdom. In the 1990’s he was involved with the digital transformation of Telecommunication infrastructure for Maxis and Telekom Malaysia. His passion for Real Estate in the 2000s led him to practice as a real estate negotiator in Ace Realty and later valuation and property management in Rahim & Co International. Several years later he founded Action Real Estate and Action Valuers & Property Consultants. His areas of expertise are in Real Estate Agency, Property Valuation, Property Management and Business Valuation. He is Member of The International Association of Certified Valuation Specialists of Canada, Member of Royal Institution of Surveyors Malaysia, Member of Malaysia Institute of Estate Agents and Member of Business Valuers Association of Malaysia.